The 50/30/20 Budget Rule: Does It Actually Work When You're Self-Employed?

- Donna Roggio

- Jun 6

- 11 min read

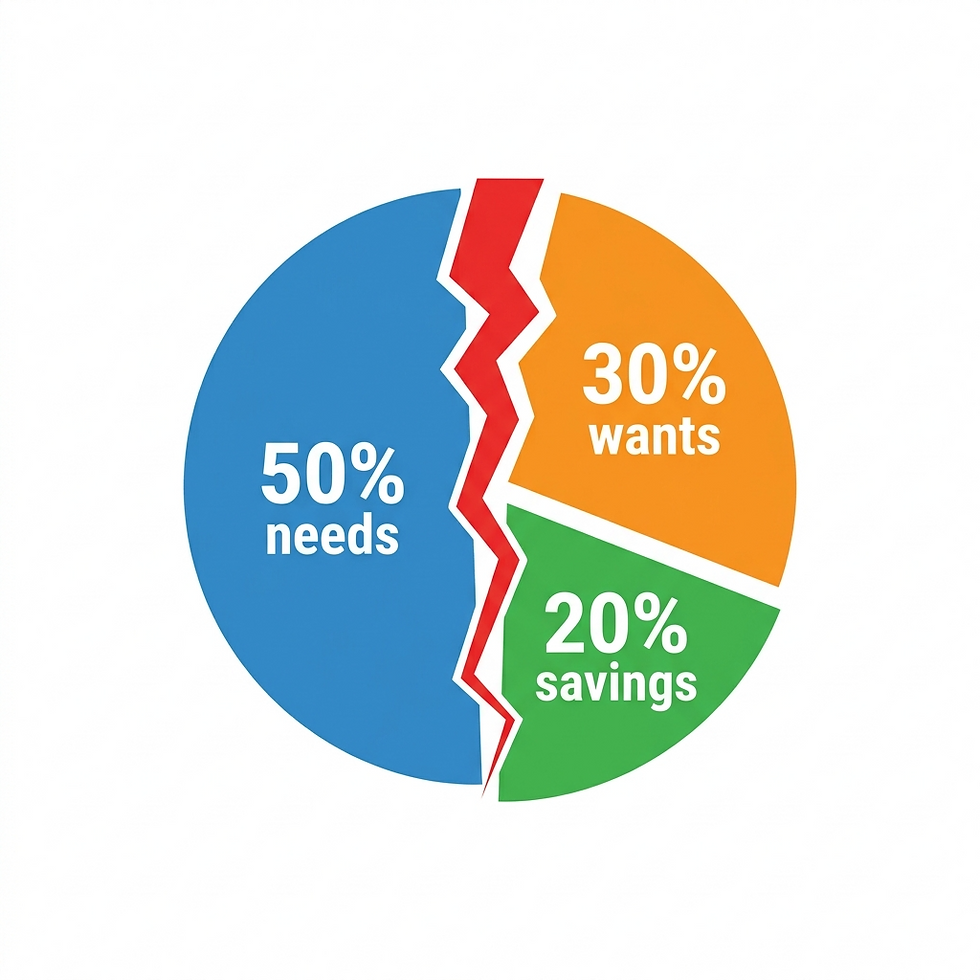

If you have ever searched "how to budget," you have probably been told to follow the 50/30/20 rule. Spend 50% of your after-tax income on needs, 30% on wants, and 20% on savings or debt repayment. It is clean, simple, and fits nicely on an Instagram infographic.

50 30 20 budget rule

But here is the uncomfortable truth that nobody posts about: the 50/30/20 rule was designed for people with a steady, predictable paycheck. If you are self-employed, freelancing, or running your own business, your income does not arrive in tidy biweekly deposits. It arrives in waves, droughts, and surprises. And trying to force a cookie-cutter formula onto that reality can leave you stressed, broke, and wondering what you are doing wrong.

You are not doing anything wrong. You just need a different framework.

In this post, we are going to break down exactly what the 50/30/20 rule is, why it falls apart for self-employed earners, and what to use instead. Because popular advice is not always the right advice, especially when your financial life does not look like everyone else's.

What Is the 50/30/20 Rule (and Where Did It Come From)?

The 50/30/20 rule was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan. The idea is elegantly simple. Take your after-tax income and divide it into three buckets:

Needs (50%) cover the non-negotiables. Housing, utilities, groceries, insurance, minimum debt payments, transportation, and anything else you truly cannot function without.

Wants (30%) cover the nice-to-haves. Dining out, entertainment, streaming subscriptions, gym memberships, vacations, and upgrades to things you already own.

Savings and Debt Repayment (20%) covers your future. Emergency fund contributions, retirement savings, extra payments on loans, and investments.

The appeal is obvious. You do not need a spreadsheet, you do not need an app, and you do not need to track every single dollar. Just keep your spending roughly within those three zones, and you are budgeting.

For a salaried employee earning a consistent paycheck, this can be a solid starting point. A 2024 Talker Research and EarnIn survey found that average Americans earning $75,000 or less actually spend about 64% on needs, 16% on wants, and 16% on savings. That means most people are already overshooting needs and undershooting both wants and savings, even with stable income. The 50/30/20 rule at least gives them a target to move toward.

But what happens when your income is not stable at all?

Why the 50/30/20 Rule Breaks Down When You Are Self-Employed

Self-employment changes everything about how money flows. According to the Federal Reserve's 2025 Economic Well-Being of U.S. Households report, 58% of self-employed adults say their income varies from month to month. That is more than double the rate for traditional employees.

And that monthly variation is not a minor inconvenience. It fundamentally undermines the math behind the 50/30/20 rule.

Here is why.

Problem 1: You do not have a consistent "after-tax income" to split.

The 50/30/20 rule starts with your after-tax income. But when you are self-employed, your taxes are not automatically withheld from a paycheck. You owe self-employment tax of 15.3% (covering both the employer and employee share of Social Security and Medicare), plus federal and state income taxes on top of that. Most tax professionals recommend setting aside 25% to 35% of your gross income for taxes alone. That money needs to come out before you even think about needs, wants, or savings. The 50/30/20 rule does not account for this at all.

Problem 2: Your "needs" percentage changes every month.

When you earn $8,000 in March and $3,000 in April, your rent does not shrink accordingly. Your fixed costs stay the same, but the percentage they consume swings wildly. In the $8,000 month, rent might be 20% of income. In the $3,000 month, it could be 50% all by itself. Trying to maintain a consistent 50% needs allocation when your income fluctuates this much is not just impractical. It is impossible.

Problem 3: Business expenses blur the lines between "needs" and "wants."

Is your coworking space membership a business need or a personal want? What about your phone bill that serves both personal and business purposes? Your laptop? Your internet service? When you run a business, the line between personal and business expenses gets blurry fast. The 50/30/20 rule was not built for that complexity. (If you have ever struggled with this, our post on how to tell the difference between a business expense and a personal expense can help.)

Problem 4: 20% savings may not be enough (or may be too ambitious) depending on the month.

In a strong revenue month, you should probably be saving far more than 20%. That surplus needs to cover the lean months ahead. And in a slow month, even 5% toward savings might feel like a stretch. A flat percentage does not adapt to the peaks and valleys of self-employed life.

Problem 5: It ignores the feast-or-famine cycle entirely.

Self-employment income is not just variable. It is often seasonal or project-based. A freelance designer might earn 60% of their annual revenue in Q4. A landscaping business might earn almost nothing from December through February. The 50/30/20 rule treats every month like it exists in isolation, when in reality, each month is funding the next.

As personal finance expert Bobbi Rebell put it, the rigid split "reflects the tough reality for many Americans in what is a very expensive inflationary environment." And when you add income volatility on top of that, the cracks get even wider.

The Real Numbers: What Self-Employment Actually Costs

Before we talk about a better framework, it helps to understand the financial reality that self-employed earners face. These numbers show why a one-size-fits-all budget rule simply cannot hold:

Self-employment tax alone takes 15.3% of net earnings right off the top (IRS). That is money a W-2 employee never sees because their employer pays half. When you combine self-employment tax with federal and state income taxes, the recommended set-aside is 25% to 35% of gross revenue (ADP Tax Calculator, TurboTax).

Housing costs are consuming more than ever. Monthly mortgage payments now average about 35% of median household income on their own (Reddit/Infographics analysis of 2025 data, Harvard Joint Center for Housing Studies). For renters, nearly 90% of families earning below $20,000 spend more than 30% of income on housing (U.S. Treasury Department).

Income volatility is the norm, not the exception. Fifty-eight percent of self-employed adults report month-to-month income variation, compared to roughly 29% of all adults (Federal Reserve SHED 2025). The difference in income growth between the 90th and 10th percentiles of self-employed workers is 2.5 to 3 times larger than for salaried workers (Minneapolis Federal Reserve, 2025).

Self-employment hit a record high of 16.77 million Americans in 2025 (Small Business & Entrepreneurship Council, citing BLS data). That means more people than ever are trying to budget with income that does not cooperate with textbook rules.

A Better Framework: The Priority Percentage Method for Self-Employed Earners

Instead of splitting your income into three neat buckets, self-employed earners need a framework that adapts to what actually comes in each month. We call this the Priority Percentage Method, and it works in layers rather than fixed slices.

Think of it like this. The 50/30/20 rule is a pie chart. Every month, the pie is the same size and every slice is the same proportion. The Priority Percentage Method is more like a waterfall. Money flows in, and you fill the most important buckets first. When more money flows in, the lower-priority buckets get filled too. When less money flows in, those lower buckets wait.

Here is how it works.

Layer 1: Taxes (25% to 30% of gross revenue)

This is always the first allocation. Before you pay rent, before you buy groceries, before you celebrate a big invoice payment. Move 25% to 30% of every dollar that hits your business account into a separate tax savings account. The IRS does not care whether you had a good month or a bad month. Quarterly estimated taxes are due regardless, and underpayment penalties add up quickly.

If you are already using the method we described in our post on small business tax deductions, you know that deductions can lower your effective rate. But it is always better to over-save for taxes and get a pleasant surprise than to scramble in April.

Layer 2: Business Operating Costs (actual cost, not a percentage)

Your business costs what it costs to run. Software, insurance, supplies, contractors, rent on a workspace. These are real, non-negotiable numbers, not a percentage you can adjust. List them, track them, and pay them.

This is where reviewing your spending leaks regularly matters. If your operating costs are creeping up and you have not noticed, every other layer suffers.

Layer 3: Owner's Pay (a set baseline amount)

Instead of taking a percentage of each month's revenue, set a baseline "salary" you pay yourself. This should be the minimum amount you need to cover your personal needs and essentials. Use your monthly financial review to determine this number.

In a $3,000 month, your baseline pay keeps you afloat. In an $8,000 month, you still take the same baseline. The difference goes to the next layers.

Layer 4: Emergency and Runway Fund (until you reach 3 to 6 months of combined expenses)

Every self-employed person needs a financial runway. Not just a personal emergency fund, but a business emergency fund. If a client ghosts, if a project falls through, if an unexpected expense lands on your desk, this is the money that keeps the lights on without forcing you into debt.

We covered this in depth in our post on building an emergency fund for your small business. Until this fund is fully stocked, surplus money from strong months should flow here before it goes anywhere else.

Layer 5: Savings and Growth (whatever remains)

This is where retirement contributions, investments, business expansion, skill-building courses, and financial goals live. In lean months, this layer might get nothing, and that is okay. In strong months, this is where you build real wealth.

The key difference from the 50/30/20 rule is that this layer is not a fixed 20%. It is whatever is left after the priorities above are handled. Some months it will be 30% or more. Other months it will be zero. And that flexibility is exactly the point.

A quick comparison:

With the 50/30/20 rule, a self-employed person earning $5,000 in a given month would allocate $2,500 to needs, $1,500 to wants, and $1,000 to savings. But that math ignores the $1,250 to $1,500 that needs to go to taxes, the business expenses that might eat another $1,000, and the fact that the "wants" bucket might need to shrink to zero in a tight month so the emergency fund can grow.

With the Priority Percentage Method, that same $5,000 flows like this: $1,375 to taxes (27.5%), $900 to business operating costs (actual), $1,800 to owner's pay (baseline), $625 to the emergency fund, and $300 to savings and growth. The numbers flex with reality instead of fighting it.

How the Profit First Method Complements This

If the Priority Percentage Method resonates with you, you will love the Profit First method created by Mike Michalowicz. Profit First flips traditional accounting on its head. Instead of Sales minus Expenses equals Profit, it uses Sales minus Profit equals Expenses.

The framework uses five dedicated bank accounts (Income, Profit, Owner's Pay, Taxes, Operating Expenses), and you allocate a set percentage of every deposit into each account. For businesses earning under $250,000 annually, Michalowicz recommends starting with 5% to profit, 50% to owner's pay, 15% to taxes, and 30% to operating expenses.

What makes Profit First powerful is the behavioral principle behind it. When money is separated into specific accounts, you naturally spend less because you only see what is available in each bucket. It is like the envelope method for your business, but with real bank accounts instead of cash-stuffed envelopes.

The Priority Percentage Method we outlined above aligns naturally with Profit First, and Money Mastery's tracking tools help you monitor all of these allocations in one place without managing five separate spreadsheets.

What About Other Budgeting Methods? A Quick Breakdown

You might be wondering how other popular budgeting methods stack up for self-employed earners. Here is an honest look.

Zero-Based Budgeting assigns every single dollar a job. Income minus all allocated spending equals zero. This method works beautifully for people who love detail, but it requires knowing your income in advance. For self-employed earners with variable revenue, it can be exhausting to rebuild the budget from scratch every month. That said, if you pair it with the lowest-income-month approach (budget based on your worst recent month and treat anything above that as surplus), it becomes much more manageable.

The Envelope Method divides cash into physical or digital envelopes for each spending category. It is fantastic for controlling discretionary spending, but it does not address tax savings, business costs, or the layered priorities that self-employed earners need to manage. Think of it as a great tactic inside a larger strategy.

The 80/20 Rule is simpler than 50/30/20. Save 20%, spend 80% however you want. For a salaried employee who just wants to make sure they are saving, this can work. For a self-employed person who needs to juggle taxes, business costs, personal needs, and irregular income, it is too vague to be useful.

The Pay-Yourself-First Method is the closest relative to what we are recommending. Savings comes out first, then you live on the rest. The Priority Percentage Method essentially takes this principle and expands it into multiple priority layers, making it specific enough for self-employed complexity.

None of these methods are bad. They just were not designed with your reality in mind. The best budget is the one you will actually use, and it needs to account for the way your money actually works.

How to Get Started This Week

You do not need to overhaul your entire financial life by Friday. But you can take three concrete steps right now.

Step 1: Know your baseline. Look at the last three to six months of income. What was your lowest month? That is your planning floor. Build your budget around that number, and treat anything above it as surplus to allocate to Layers 4 and 5.

If you need help pulling this together, our post on how to budget with irregular income walks you through the entire process.

Step 2: Separate your money. At minimum, open a dedicated tax savings account and a dedicated emergency fund account. When income arrives, move 25% to 30% into taxes immediately. Non-negotiable. No exceptions. If you want the full Profit First setup, open all five accounts and start with even 1% to profit. The habit matters more than the amount.

Step 3: Track for 30 days using the Priority Percentage Method. Write down every dollar that comes in and assign it to a layer. Taxes first, then operating costs, then owner's pay, then emergency fund, then savings and growth. At the end of 30 days, you will have a clear picture of where your money actually goes and how much flex you have.

Money Mastery's dashboard makes this ridiculously simple. It auto-categorizes your transactions, shows you month-over-month changes, and lets you set custom allocation layers that match this exact framework. No more guessing, no more spreadsheet gymnastics, just clarity.

Ready to get your budget working for the way you actually earn? Download our free Starter Kit and get a 15-minute financial clarity guide, a priority allocation worksheet, and a monthly review template built specifically for self-employed earners.

Frequently Asked Questions

Is the 50/30/20 rule completely useless?

Not at all. For someone with a stable salary and straightforward finances, it is a perfectly fine starting point. The problem is not the rule itself. The problem is applying it to a financial situation it was never designed for. If your income is variable, your expenses blur between personal and business, and your tax obligations are complex, you need something more flexible.

What percentage should self-employed people save?

There is no single right answer because it depends on your income level, your business stage, and how padded your emergency fund already is. A general starting point: aim to save a minimum of 20% of your gross revenue across taxes, emergency fund, and long-term savings combined. In strong months, push that to 30% or more. The Priority Percentage Method helps you prioritize where those savings go.

How do I budget when I genuinely have no idea what next month's income will be?

Use your lowest recent month as the baseline. Budget as if that is all you will earn. Anything above that number gets distributed to your emergency fund and savings layers. Over time, as you track your income patterns, you will start to see seasonal trends that make planning easier. Our post on budgeting with irregular income goes deep on this.

Should I use Profit First or the Priority Percentage Method?

They are not competing systems. Profit First gives you the account structure and the behavioral framework (separate the money so you do not spend it). The Priority Percentage Method gives you the allocation logic (which layers to fill first when income fluctuates). Used together, they are powerful. Start with whichever feels more approachable and layer in the other over time.

What if I have already been using 50/30/20 and it is not working?

You are not failing. The framework is failing you. Take 30 minutes this week to map your last three months of income and expenses using the Priority Percentage Method layers. You will likely discover that you have been trying to fit variable reality into a fixed formula, and the relief of switching to something that actually fits can be immediate.

Comments