Debt Snowball vs Debt Avalanche: Which Payoff Method Actually Works?

- Donna Roggio

- 3 days ago

- 7 min read

Debt snowball vs debt avalanche comes down to one honest question: do you need momentum or math? The snowball method pays smallest balance first for psychological wins. The avalanche method pays highest interest rate first to save the most money. A 2012 Kellogg School of Management study found snowball users were significantly more likely to eliminate their debt entirely, because finishing one debt fuels the next.

The best payoff method is the one you'll actually finish.

If you've been carrying debt for a while, you've already run the numbers more times than you can count. You know what you owe. You know the rates. You know something has to give. What you don't know yet is which method will work for you, not in theory, but in the actual reality of running a business, paying bills, and trying to stay sane while you do it.

By the end of this post you'll know exactly how each method works, see them side by side with real numbers, and have a clear way to pick the one that fits your personality and your money.

How the Debt Snowball Method Actually Works

The debt snowball method orders your debts from smallest balance to largest, regardless of interest rate. You pay the minimum on every debt except the smallest one. On that smallest debt, you throw every extra dollar you can find. When it's gone, you roll its payment into the next smallest balance. Then the next. Each payoff makes the following one feel faster, even when the math says it isn't.

The whole point is momentum. Behavioral research, including the Kellogg study above, shows that people who experience small wins early are much more likely to stay with a long plan. Debt payoff is rarely a six-month sprint. It's usually a one-to-five year stretch, and the people who finish are almost always the ones who felt themselves winning along the way.

This is the method I recommend most often to clients who've started and quit before. The reason they stopped wasn't a math problem. It was burnout. The snowball fights burnout with closed accounts and crossed-off lines on the list.

How the Debt Avalanche Method Actually Works

The debt avalanche method orders your debts from highest interest rate to lowest, regardless of balance. You pay minimums on everything except the highest-rate debt, where you focus every extra dollar. When that one is gone, you move to the next-highest rate. Then the next.

The avalanche saves you the most money over time, sometimes thousands of dollars depending on your interest rate spread. According to the Federal Reserve, the average credit card APR in early 2026 sits above 21%, while personal loans average closer to 12% and federal student loans hover around 6 to 8%. Attacking the 21% debt first beats attacking the smallest balance every time, on paper.

The catch is that paper doesn't pay debt. People do. If your highest-rate debt also happens to be your largest, you might spend two years chipping at it without crossing a single debt off the list. That's where avalanche loses people. The math is right. The motivation runs out.

Debt Snowball vs Debt Avalanche: Side-by-Side Comparison

Here's the reference asset worth screenshotting. Same starting position, two different methods, real numbers.

Sample debts:

Credit Card A: $1,200 balance, 22% APR, $35 minimum

Personal Loan: $4,500 balance, 11% APR, $120 minimum

Credit Card B: $8,000 balance, 24% APR, $200 minimum

Available extra payment per month: $300

Factor | Debt Snowball | Debt Avalanche |

First debt attacked | Credit Card A ($1,200) | Credit Card B (24% APR) |

First debt paid off | Around month 4 | Around month 18 |

Total time to debt-free | ~33 months | ~31 months |

Total interest paid | ~$2,940 | ~$2,610 |

Savings vs the other method | $0 | ~$330 |

Payoff wins in first 6 months | 1 | 0 |

Best for | People who need visible progress | People motivated by math |

Biggest risk | Slightly more interest paid | Burnout before any win |

The avalanche saves about $330 in this example. Real situations vary, sometimes savings reach the thousands. But notice that the snowball produces a full payoff in month 4, while the avalanche has zero payoffs until month 18. For most people, that 14-month gap is where the plan dies.

How to Pick the Method That Fits You

Here's the part nobody tells you. The right method isn't about being smart enough for avalanche or weak enough for snowball. It's about honest self-knowledge. Use this if/then framework:

If you've tried debt payoff before and quit, choose the snowball. You don't need more math. You need a win.

If you're highly disciplined, run your business on spreadsheets, and feel motivated by saving money over time, choose the avalanche.

If your smallest debt and your highest-rate debt are the same debt, the methods are identical for your first payoff. Either works.

If your highest-rate debt is also your largest, lean snowball. Two years without a visible win is the fastest way to abandon ship.

If you only have one or two debts, the choice barely matters. Pick one and start.

Whatever you choose, get your spending clear first. You can't put $300 extra toward debt if you don't know where your $300 currently goes, which is exactly what the how to track where your money goes guide walks through step by step.

The Hidden Third Option: A Hybrid Approach

There's a method nobody talks about, and it's the one I use with most of my clients. Start with one small snowball win to build momentum, then switch to avalanche for the rest.

Here's how it works. Pick your smallest debt and pay it off as fast as humanly possible, even if its interest rate is the lowest in your stack. Close that account. Feel that win. Then reorder your remaining debts by interest rate and run avalanche from there.

You get the psychological lift of an early payoff and most of the math savings of the avalanche method. It's not pure either way, but it's pragmatic, and it's what works for real humans who need both motivation and money saved.

This is educational, not financial advice. Your debt situation is specific to you, and decisions like consolidation or refinancing should involve a fee-only financial planner.

What Most People Get Wrong About Debt Payoff

Most debt payoff plans fail before they really start, and it's almost never the method's fault. It's one of these three mistakes.

People keep adding new debt while paying off old debt. The card finally clears a $40 balance and then a $300 purchase shows up the next week. The math never moves. Before you start any payoff method, decide the cards are paused. Not cut up necessarily, just paused. And remember, paying the card down isn't the same as the original purchase being an expense, which is why understanding why your credit card payment is not an expense changes how you see the whole picture.

People don't know their real numbers. They estimate balances, guess interest rates, and skip the part where they list everything in one place. You can't beat what you can't see. The monthly financial review checklist is the simplest way to build the habit of looking at the full picture once a month.

People treat debt payoff as a separate budget from the rest of their life. It isn't. It's part of your monthly cash flow, your business income variability, and your personal spending. Treating it like a side project guarantees it stays a side project. Creating a place for debt in your main financial system, as Money Mastery is built to do, makes debt payoff a default part of every month rather than something you keep forgetting to look at.

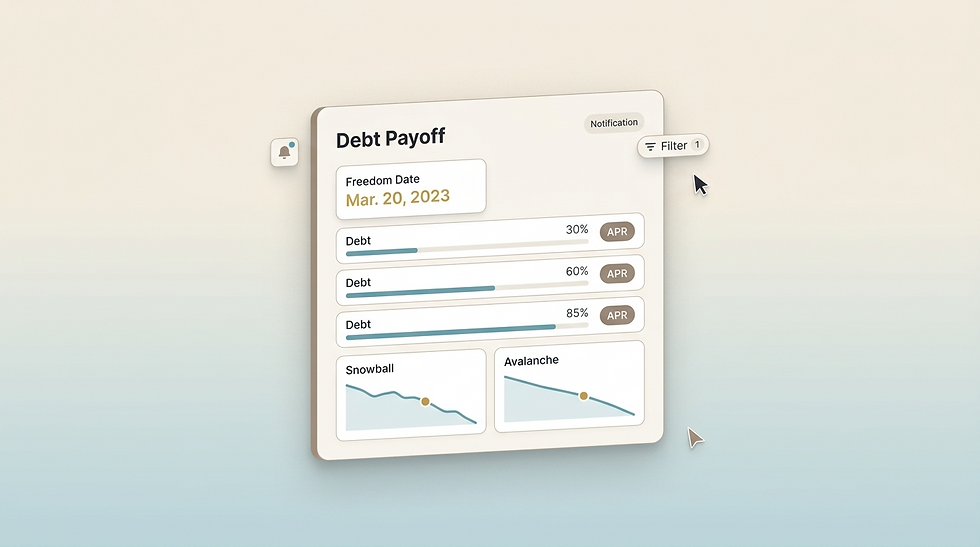

How Money Mastery Helps You Run Either Method

Money Mastery includes a debt payoff dashboard that lets you list every debt with its balance, interest rate, and minimum payment, then visually project your freedom date under both the snowball and avalanche orderings. You see, in real numbers from your real situation, what each method would cost you in time and interest. That's the difference between picking a method from a generic blog example and picking one based on what your debts actually look like.

The system also tracks your progress month over month, so the next time you wonder if you're actually making a dent, the answer is a number on a screen instead of a feeling.

Your Next Step

Pick one method this week. Not the perfect method. Just one. Write your debts on a sheet of paper. Decide what your extra payment amount is. Start next payday. The method matters less than starting, and starting matters more than almost anything else you can do for your financial life this year.

Get the free Starter Kit here: https://moneymastery-system.com/starter-kit

Frequently Asked Questions

Is debt snowball vs debt avalanche better for paying off credit card debt?

Debt snowball vs debt avalanche both work for credit card debt, but the right choice depends on your card balances and rates. If your highest-rate card is also your smallest balance, the methods are identical. If your highest-rate card is your largest balance, snowball gives you a faster first win and helps prevent burnout. Avalanche saves more money if you have several cards with widely different interest rates and the discipline to wait for your first payoff.

How long does it take to pay off debt with the snowball method?

Most people using the debt snowball method become debt-free in 18 to 60 months, depending on total debt, income, and extra payment amount. The first debt is usually gone within 3 to 6 months, which is the whole point of the method. After that, each payoff happens faster because you roll the previous minimum payment into the next debt. The total time is similar to the avalanche method, usually within a few months either way.

Does debt avalanche actually save that much money?

Sometimes yes, sometimes barely. Debt avalanche saves the most when you have a large gap between your highest and lowest interest rates, like a 24% credit card alongside a 5% student loan. In that case, savings can reach the thousands. If your debts are within a few percentage points of each other, avalanche might only save you $100 to $400 over the life of the payoff, which is often not worth losing motivation over.

Can I switch methods partway through paying off debt?

Yes, and many people do. A hybrid approach starts with one snowball win to build momentum, then switches to avalanche for the remaining debts. There's no penalty for switching. The only real risk is decision fatigue, where you keep changing methods instead of paying. Pick a method, commit to it for at least one full payoff, then reassess. Money Mastery's debt payoff dashboard lets you compare both methods on your real numbers before you switch.

What's the best app or tool to track debt snowball vs debt avalanche progress?

The best tool is one that shows your full financial picture, not just your debt. Most debt-only apps disconnect your payoff from the rest of your spending and cash flow, which is where most debt payoff plans actually fall apart. Money Mastery includes a debt payoff dashboard built into a complete financial clarity system, so your debt progress lives alongside your income, expenses, and savings. That integration is what makes the plan stick.

Comments